{kind=link}

Earlier this week, I joined Ciena and Telstra for a stay webinar highlighting Asia-Pacific market drivers, developments, and new cable builds.

Throughout my session, which centered on Trans-Pacific submarine cable developments, content material suppliers got here up fairly a bit.

These firms prioritize the necessity to hyperlink their information facilities and main interconnection factors. As such, they typically deploy large quantities of capability on core routes.

The Trans-Pacific and Intra-Asia routes are two nice examples.

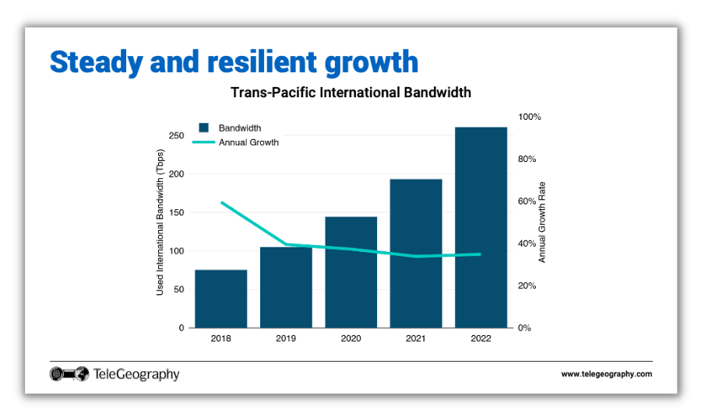

I started my presentation by displaying Trans-Pacific worldwide bandwidth from 2018 to 2022.

This chart reveals that bandwidth demand progress throughout the Pacific has remained resilient and reasonably regular through the years. Trans-Pacific bandwidth grew 35% year-over-year in 2022 alone, reaching simply over 250 Tbps of capability.

Though the turquoise line reveals a dip in annual progress earlier than stabilizing in 2019, the extra essential takeaway is absolutely the improve in wholesome bandwidth progress through the years.

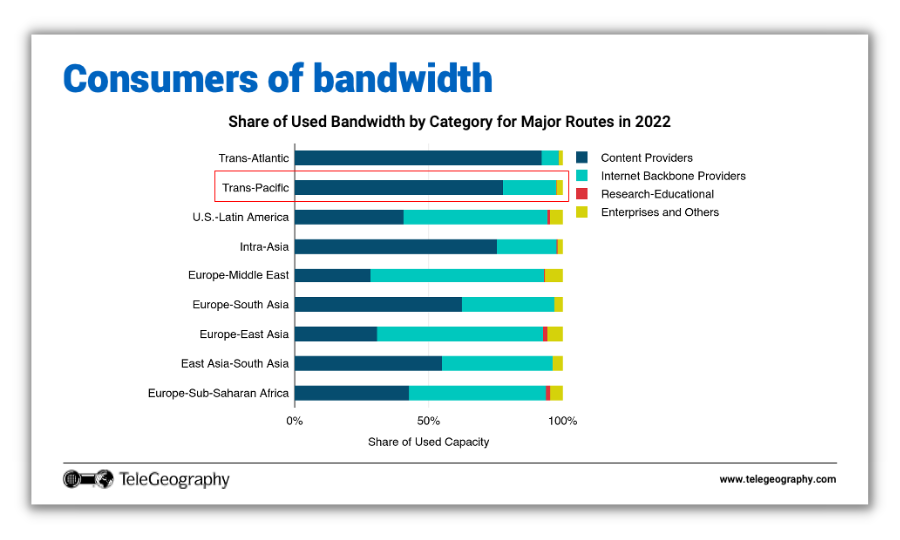

And who’s consuming all of this bandwidth?

The slide beneath breaks down 4 totally different classes of bandwidth customers—Content material Suppliers, Web Spine Suppliers, Analysis-Instructional, and Enterprises and Others—throughout a number of main routes.

We will see that bandwidth utilization just isn’t evenly distributed throughout these classes.

Content material suppliers, proven in navy blue, take up enormous shares of capability throughout the Pacific and Intra-Asia (roughly greater than 78% and 75% of bandwidth, respectively).

On the flip aspect, web spine suppliers (turquoise), nonetheless eat bigger volumes of bandwidth on sure routes, like U.S.-Latin America, Europe-Center East, and so forth.

With that being stated, we anticipate a common improve in content material supplier share of bandwidth throughout most of those routes within the years to come back. Demand from different forms of customers can be rising, simply not as quick as content material supplier demand.

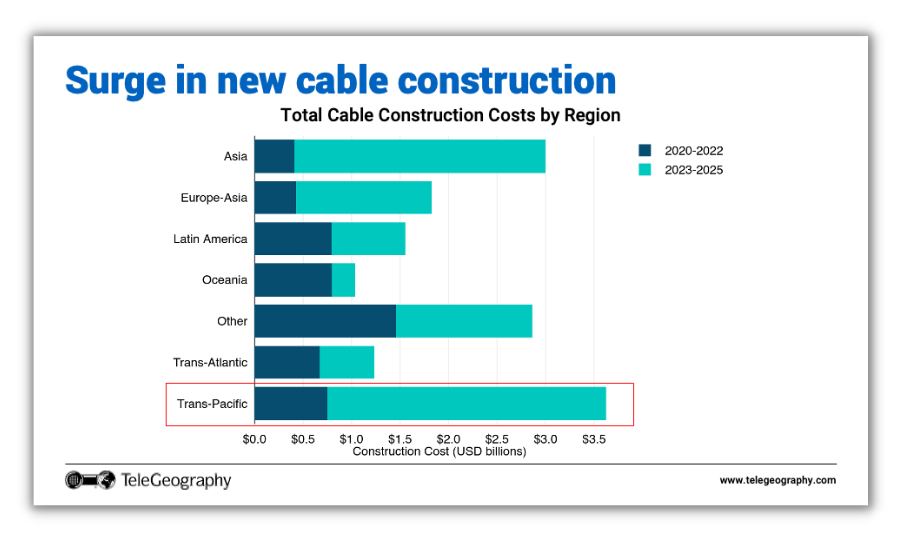

Unsurprisingly, the rise in bandwidth demand has led to a surge in new cable funding.

Unsurprisingly, the rise in bandwidth demand has led to a surge in new cable funding. As we will see within the determine beneath, there are quite a lot of cables coming into service within the subsequent three years.

Specializing in the Trans-Pacific alone, the development worth for cables coming into service from 2023-2025 is considerably larger in comparison with 2020-2022.

We additionally witness equally excessive ranges of cable funding in Asia—also called Intra-Asia—as there’s a must distribute this capability inside the area. Word that there could also be extra, unannounced cables on the horizon, which can additional inflate these values.

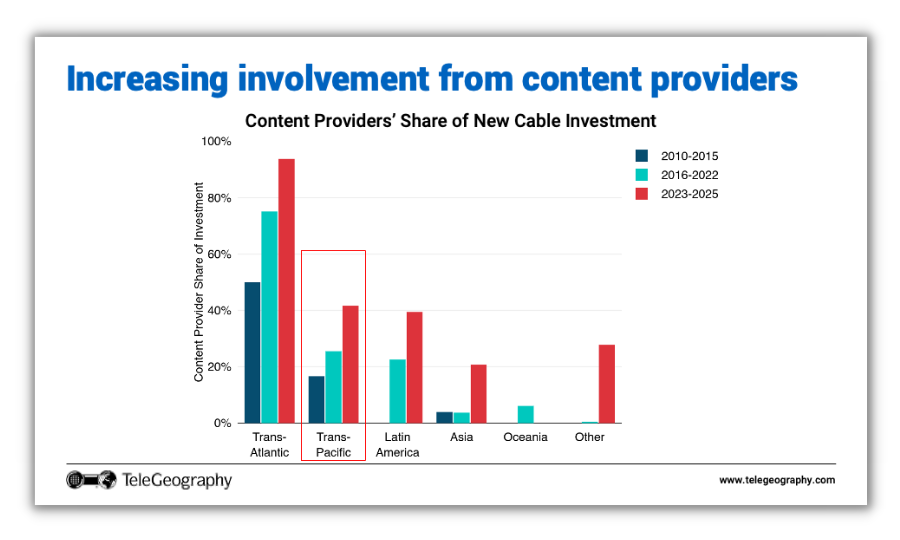

Earlier in my presentation, I established that content material suppliers eat extra bandwidth on sure routes.

If we break down content material supplier funding in new cables by time interval, we see will increase throughout the board.

Practically half of all Trans-Pacific cable investments coming into service between 2023-2025 are backed and funded by content material suppliers.

Practically half of all Trans-Pacific cable investments coming into service between 2023-2025 are backed and funded by content material suppliers.

And we consider that this pattern is prone to improve sooner or later.

Subsequent, my presentation coated why world value erosion is slowing, the truth of U.S. and China decoupling, and an outline of all previous and new cable programs throughout the Pacific.

If you need to discover these subjects, you’ll be able to obtain my slides over right here. An on-demand recording of the complete webinar can be obtainable to observe right here.