{kind=link}

A couple of years in the past, Neel Augusthy—a forensic accounting knowledgeable at Toptal, who has held regional and divisional CFO roles at Medtronic and Johnson & Johnson—was reviewing an organization’s efficiency on the request of its proprietor, a conglomerate. As is typical for forensic accounting professionals, he blends each quantitative strategies and qualitative instruments resembling conversations, behavioral observations, and website visits in his work.

Augusthy started that exact investigation, as he typically does, by reviewing audits of comparable firms. He discovered that the corporate was a lot much less worthwhile than others prefer it and that its profitability didn’t line up with expenditures—each crimson flags. His subsequent transfer was to spend a big period of time speaking and listening to staff and distributors of the corporate.

Asking questions is essential to getting individuals to divulge heart’s contents to you, he says. “You nearly must be childlike, asking out of pure ignorance: ‘Are you able to clarify to me how that works? You’re telling me this, and my different supply over right here is telling me that, so how does all of it match collectively?’”

When Augusthy talked to the corporate’s distributors, many complained about low margins, which didn’t make sense, given how a lot the corporate claimed it was paying them. So he took the corporate’s basic supervisor to dinner, below the pretense of catching up and discussing potential enhancements.

“When individuals speak they usually really feel comfy, they inform you numerous issues they in all probability shouldn’t,” says Augusthy. “I requested [the GM] why the distributors had been complaining about margins being so low once we pay them a lot. He stated, ‘Oh, these guys simply hold complaining for no motive.’” The GM made another feedback that felt off to Augusthy too: “He’d simply ‘purchased this piece of land right here’ and ‘that one there.’ And I assumed: This isn’t including up. Out of the blue he’s obtained some huge cash to make these purchases.”

“That’s once I discovered he had been skimming from the enterprise by taking cash that was because of the distributors,” Augusthy says. Because of the investigation, the conglomerate eliminated the supervisor and improved checks and balances to ensure it didn’t occur once more.

What Is Forensic Accounting?

Forensic accountants, additionally known as investigative accountants, are generally related to investigating legal exercise, however that’s not all they do. These specialised practitioners are geared up with particular accounting expertise and instruments to dig into what lies beneath monetary statements and uncover different hidden issues and dangers, together with these associated to:

- Fraud: lack of capital because of wrongful or legal deception.

- Regulatory compliance: taxes or fines because of a failure to abide by legal guidelines.

- Liquidity: lack of capital because of extreme debt and inadequate fairness.

- Funding: lack of capital because of investing in a troubled enterprise.

- Credit score: lack of capital because of lending cash to a borrower who’s unable to repay.

Within the greater than 20 years for the reason that scandals and collapses of Enron and WorldCom catalyzed the introduction of the Sarbanes-Oxley Act, the company threat surroundings has change into extra risky and sophisticated. The velocity of technological innovation, the disruption of provide chains, and the looming local weather disaster not solely make it more durable to anticipate monetary threat, the elevated volatility additionally gives fertile floor for fraud.

Whereas conventional monetary threat evaluation strategies will be efficient in figuring out and mitigating many issues, they’re not all the time adequate to uncover all forms of monetary threat. Given the enterprise surroundings, there’s a harmful underutilization of forensic threat evaluation and administration, particularly amongst small to medium-size companies, says Toptal Chief Economist Erik Stettler. In his earlier work for NERA Financial Consulting, he studied the failures and near-failures of a lot of outstanding US establishments throughout the Nice Recession.

Many firms attempt to save cash by working less-rigorous checks with in-house employees, Stettler says, however that’s dangerous as a result of staffers might not have the mandatory expertise or could also be so accustomed to the best way enterprise is finished on the firm that they fail to see crimson flags. Failing to determine fraud, violating rules, or shrinking liquidity value an organization way over the upfront capital outlay for specialised investigative accounting, which usually ranges from $30,000 to $50,000 per venture, he says. In distinction, a December 2017 research of multinational organizations discovered that the common annual value of noncompliance was practically $15 million.

Forensic Accounting for Monetary Danger Evaluation

Investigative accountants do greater than study monetary statements. These specialists method investigations holistically, incorporating statistical evaluation, market analysis, images or visible inspections of amenities, conversations with human sources, and research of people’ and firms’ histories, behaviors, and psychology to uncover the reality. For instance, to look at a enterprise’s revenue or bills, somewhat than simply have a look at annual or quarterly financials, forensic accountants might ask for real-time numbers for the time interval in query to be able to observe fluctuations in additional element.

“When contemplating a mortgage, an funding, or an M&A deal, or when conducting an audit, it’s crucial to take a extra granular look past conventional financials and in addition seek the advice of, in depth, different sources of details about an organization,” Stettler says. However threat managers can’t simply ship a forensic accountant on a fishing expedition to see what they flip up. Forensic accounting is a big funding and requires that there be particular claims or issues to analyze.

A threat administration framework can present firms with a structured method to figuring out, assessing, and mitigating numerous forms of threat, together with whether or not to interact a forensic accountant to dig deeper. When the framework flags monetary irregularities, resembling unusually excessive compensation exercise by debtors, it would set off a forensic investigation. That’s as a result of larger compensation figures point out a big enhance in income for the borrower. A forensic accountant would examine whether or not that sudden windfall may very well be tied to fraud. Let’s look extra intently at how investigative accounting strategies can apply in three main threat areas.

Forensic Accounting and Fraud Danger

When trying into questions of fraud, investigative accountants sometimes ask themselves what they might anticipate to see if all is properly, simply as a doctor may evaluation a affected person’s vitals with a “regular” benchmark in thoughts. Then they assess statistically whether or not what the corporate is reporting matches up, Stettler says.

Simply as Augusthy did, investigative accountants additionally have a look at whether or not sure transactions or monetary statements are based mostly on persuasive financial and monetary logic. If a monetary report experiences that an asset was offered for 100 instances greater than comparable transactions or an impartial valuation suggests, the transaction should still be legitimate within the strict sense of the phrase—nevertheless it represents a suspiciously giant departure from financial logic. In that case, not solely ought to that transaction be scrutinized however so ought to others, to see if there’s a sample.

When investigative accountants have historic knowledge, one other key step is taking a look at statistical structural breaks, resembling modifications in the best way that an asset was priced or in how money flows or earnings occurred. “This typically entails trying on the correlation of economic or inventory value efficiency versus benchmarks and seeing if there’s a level at which the connection breaks down or modifications, that means monetary exercise throughout the firm is now being pushed by one thing aside from market components,” Stettler says.

Evaluating earnings historical past towards analyst consensus expectations is one other tactic. When firms constantly beat consensus by a small margin, that success might mirror reliable selections associated to depreciation or when to acknowledge income, however it could additionally trace that they’re managing their earnings to provide monetary statements that mirror a rosier image. Both means, Stettler says, a constant margin like this could sign a necessity for a more in-depth look.

Forensic Accounting and Regulatory Compliance Danger

Relating to staying in full compliance with authorities rules, firms face a spread of dangers, together with these associated to disclosure, minimum-wage legal guidelines, mandated day without work, and tariff and commerce coverage modifications. These dangers are notably acute when an organization maintains a presence in a couple of state or nation.

With rising acceptance of distant work, an increasing number of firms face important regulatory compliance dangers tied to work-from-anywhere preparations, explains Toptal finance specialist and distant work knowledgeable John Lee. These compliance dangers, which may end up in important financial losses, contact on a variety of areas, together with taxes, immigration, insurance coverage, expertise administration and advantages, and knowledge privateness and safety.

For the reason that COVID-19 pandemic, companies are taking better benefit of distant work expertise swimming pools outdoors of their speedy metro areas. However relevant tax legal guidelines are advanced and differ from nation to nation and state to state, Lee says, and firms that supply sturdy distant work alternatives would do properly to enlist forensic accountants to evaluate and assist mitigate monetary dangers related to cross-border hiring and digital nomad staff.

For instance, an organization might incur further company or revenue tax burdens if an worker stays in a foreign country or state lengthy sufficient to inadvertently set up residence there. Furthermore, an worker’s prolonged keep might even represent a everlasting institution of the enterprise in that space. Any firm seeking to put money into, merge with, or purchase a agency with distant work insurance policies must also rent a number of forensic accountants to make sure the companies are in compliance with tax and employment rules, Lee says.

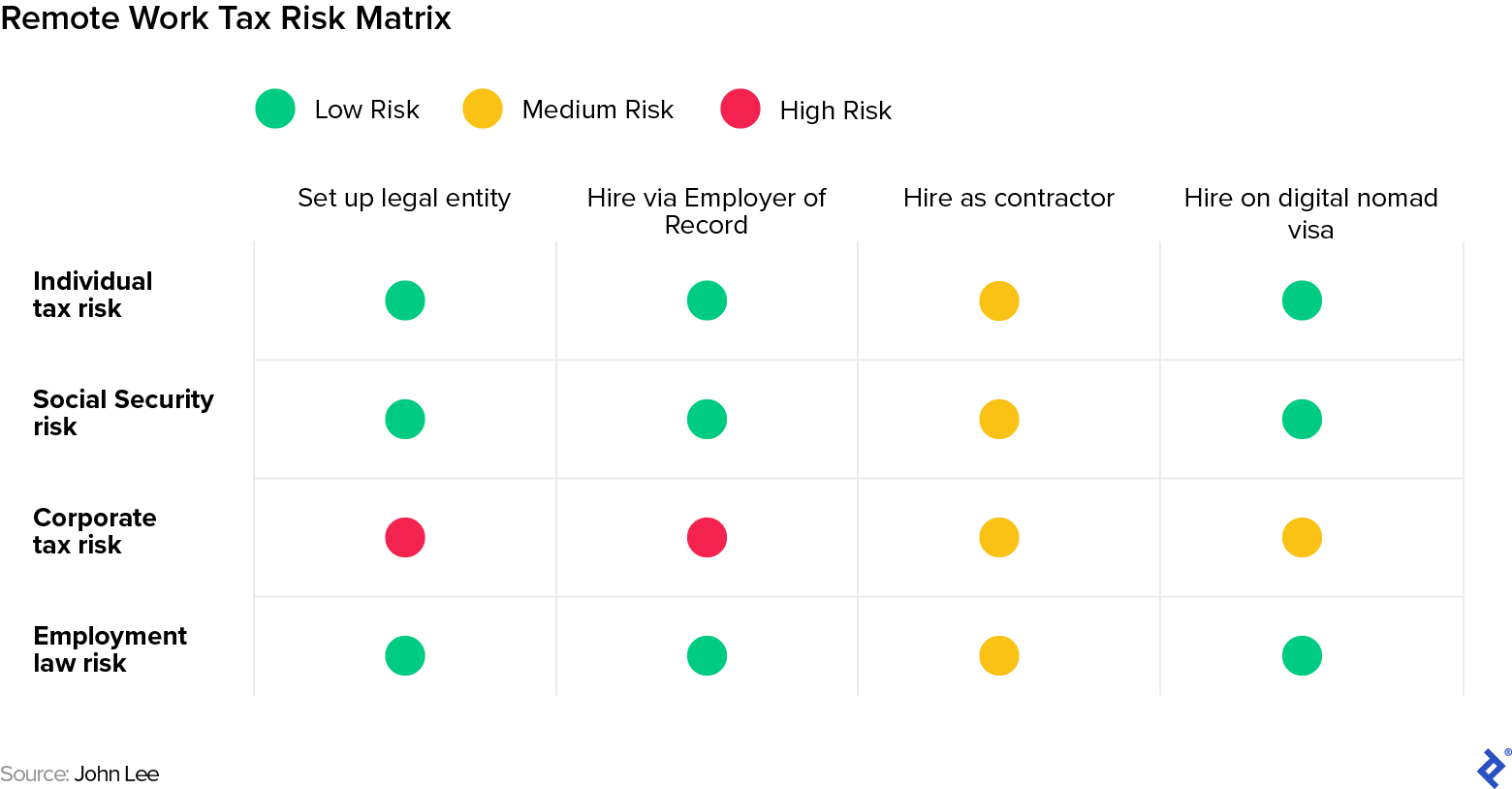

To assist firms with distant staff handle regulatory compliance, threat professionals use a distant work tax threat matrix that exhibits the person tax, company tax, Social Safety, and employment regulation dangers of actions, together with establishing a authorized entity, hiring through an Employer of Report, hiring a contractor, and using a employee on a digital nomad visa.

Forensic accountants are uniquely certified to search out potential tax dangers concerned with distant work and advise firms as to when they should seek the advice of a tax knowledgeable for a selected nation, Lee says. “No one is predicted to abruptly be a tax knowledgeable in each nation on this planet. However on the similar time, if the corporate has 15 senior gross sales individuals spending six months working within the south of France, or in case your CTO is employed through an Employer of Report, then it’s worthwhile to a minimum of flag that that is one thing that probably requires tax experience.”

Forensic Accounting and Liquidity Danger

Having investigative accountants try an organization’s books as a stress take a look at—a lot as white-hat hackers attempt to breach company networks—is a great solution to mitigate liquidity threat, Stettler says. He’s change into an advocate for such a proactive method after spending years analyzing main crises and disruptions within the securities markets and personal transactions. At any time when one in every of these occasions occurred, NERA Financial Consulting, the agency he labored for, would look into what had actually occurred versus what ideally ought to have occurred.

When Stettler helped examine a big US financial institution that collapsed throughout the subprime mortgage disaster, he carried out a deep dive into the corporate’s transaction portfolios, the chance ranges their counterparties had accepted, and the way conscious of the chance these counterparties had been or ought to have been. He additionally regarded into whether or not the dangers taken had been according to the financial institution’s said frameworks for leverage and asset diversification.

“Our function in instances just like the collapse of that financial institution was additionally to assist the counterparties perceive their publicity to the chance of fallout from the catastrophe,” he says. “CEOs of among the world’s largest monetary establishments had little concept what their degree of vulnerability was.” That’s as a result of their portfolios and hedging methods had been so advanced and different that it was not possible to embody them adequately within the typical top-line monetary statements, he explains.

There have been additionally managerial selections that inadvertently created vulnerabilities. Within the case of the aforementioned financial institution Stettler was investigating, an intense quarterly efficiency evaluation course of incentivized staff to set terribly excessive targets that allowed unexamined threat to build up beneath the floor. Nobody thought to look at whether or not that incentive construction may create ripple results all through the financial institution’s operations and transactions. The financial institution’s threat formulation had been additionally a part of the issue, since they vastly underestimated the chance of housing costs declining collectively and at such a magnitude. For the very best outcomes, these threat analyses ought to have been carried out by outdoors specialists utilizing completely different fashions to keep away from catastrophic blind spots, Stettler says. Surfacing these dangers would have empowered firms to deal with them earlier than they turned an issue.

Going ahead, he says, as enterprise struggles to maintain up with evolving expertise and regulation, it’s probably that the Worldwide Monetary Reporting Requirements, or principles-based accounting, will more and more dominate rules-based accounting, as embodied within the US method known as Usually Accepted Accounting Ideas (GAAP).

For the reason that principles-based technique gives a extra refined and adaptable means to convey underlying financial fact and includes deeper questions than which containers have been checked, monetary threat evaluation will in all probability require extra investigative accounting. And that, Stettler believes, is a giant a part of why demand for these providers is rising, a pattern he predicts will proceed.